Pharmacy Metrics, The First 6 Months of COVID-19

July 29, 2020

Rx metrics – The first six months of COVID and pharmacy finances

As published in PharmacyU

Earlier in the year, we reported on the economic implications facing pharmacists and pharmacies during the first four months of the COVID-19 pandemic. In summary, January and February prescription revenue, profit, and numbers were relatively unaffected and were comparable to 2019. March onward was a completely different story, however, and we stated that “March borrowed from April.” While March totals were higher than the same period in 2019, April was dismally low. Gross profit margin percentages in April, though, were up, and profitability was muted, but not as much as one would have expected based on the significant drop in prescription counts (on an aggregated basis of the study group). The following article is our followup.

Ostensibly, the bump in script counts in March we attributed in part to a bit of hoarding, and April numbers suffered as a result. Prescription gross margin in April improved due to the 30-day fill policy in many parts of the country. We submit that the May stats gave us a glimpse of what pharmacy revenue and profitability would look like if 30-day fills were the new normal. The timing of the return to dispensing three-month supply came in June, and as a result, many pharmacies spoke of unprecedented workload in their pharmacies in the last weeks of June and the first couple weeks of July. It is those patients who had filled their 100-day prescriptions in March reappearing, coupled with the those who were on 30-day fills in April and May clustered into a 30-day window (late June to early July). We anticipate July will continue to resemble June, with lulls in August and the first two weeks of September. These lulls will be followed by a return of a spike in the last weeks of September and the early weeks of October. We anticipate the rush to be over just in time for flu shot season.

Depending on how schools reopen in September, the cough and cold business will somewhat mute the expected spike. Even in the unlikely event that schools open in a quasi-normal fashion, we believe sanitation and hygiene rituals and distancing will affect the infection rates of other illnesses. If the above is true, mid-December will spike again, but at this time, the cycling will be somewhat flattened.

Chart 1 below is a visual prelude to the cycle:

Source: EVCOR – Enterprise Valuators Corporation

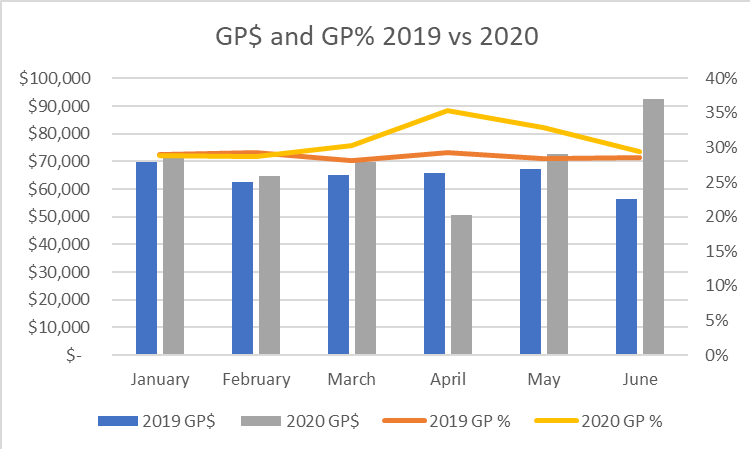

Let’s consider profitability and margin throughout this period. Revenues and margins in Chart 2 speak for themselves, and June is somewhat reflective of what happens when the bulk of your patients need their prescriptions in the same month. The drop in margin percentage back to normal levels in June is due in part to the return to 100-day fills.Source: EVCOR – Enterprise Valuators Corporation

Chart 2

Source: EVCOR – Enterprise Valuators Corporation

So what, you ask? All of this is somewhat intuitive, and those watching their numbers might have been able to predict this. What makes these statistics interesting is comparing the same stores to the same periods in 2019 – as seen in Chart 3 below. COVID-19 has had devastating effects on many sectors of our economy, but has been positive for the dispensary. Despite the April drop, the first six months of 2020 represent a 9% increase in gross profit dollars over 2019. We are not oblivious to the fact that variable expenses have grown during this period as well, which has softened net profitability.

Chart 3

Source: EVCOR – Enterprise Valuators Corporation

In our earlier article, we invited feedback regarding the COVID-19 impacts on your pharmaceutical supply chain, profitability, and staffing. Based on the results, we believe that at the time, pharmacists might not have considered that at some point, there would be an inflection point – when most of their regular customers would be returning within the same month. In fact, the majority of the survey respondents said they strongly disagreed that there would be an unmanageable staffing situation. Both anecdotally and empirically, this appears not to have been the case in June and early July. Pharmacists are feeling burned out by the spike.

Furthermore, at the time of the survey, respondents did not agree that there would be an aperiodic and potentially unmanageable revenue stream for their pharmacy. Now with the data, we can see early evidence of an oscillating revenue and resultant workload cycle for pharmacy operators. The only thing that could be considered agreement from respondents was that without a phased approach to reintroducing 100-day fills, drug shortages would worsen. However, the “phasing in” ship has sailed, and we’ll have to wait and see the impact on drug shortages.

The first six months of COVID-19 have been hard on frontline pharmacy workers but have also shown us that pharmacy can and will prevail. They have also demonstrated that our supply chain remains precarious and fragile and should not be taken for granted. It behooves us as a profession to ensure that our policymakers and payers avoid decisions that further exacerbate the situation.

Max Beairsto, B.Sc. Pharm., MBA, CVA is an intermediary and valuation analyst with EVCOR (Enterprise Valuators Corporation), a Canadian business advisory firm that focuses on valuations and the sale of healthcare-related companies.

Coming to Market:

Western Canada

Max Beairsto, BSc., MBA, CVA

max@evcor.com

www.EVCOR.com

1-844-283-6367 ext 101

Dan Reich, PharmD.

dan@evcor.com

www.EVCOR.com

1-844-283-6367 ext 106

to register as a buyer click here

EVCOR Advisor to “Project Loch Ness”

Congratulations Gentlemen, on your recently completed transaction

Check out EVCOR’s pharmacy advisor programs

Grow your business with sage advice with EVCOR’s advisory network

Proudly supporting: